Featured Articles

PG Calc publishes monthly articles on the latest topics in planned giving.

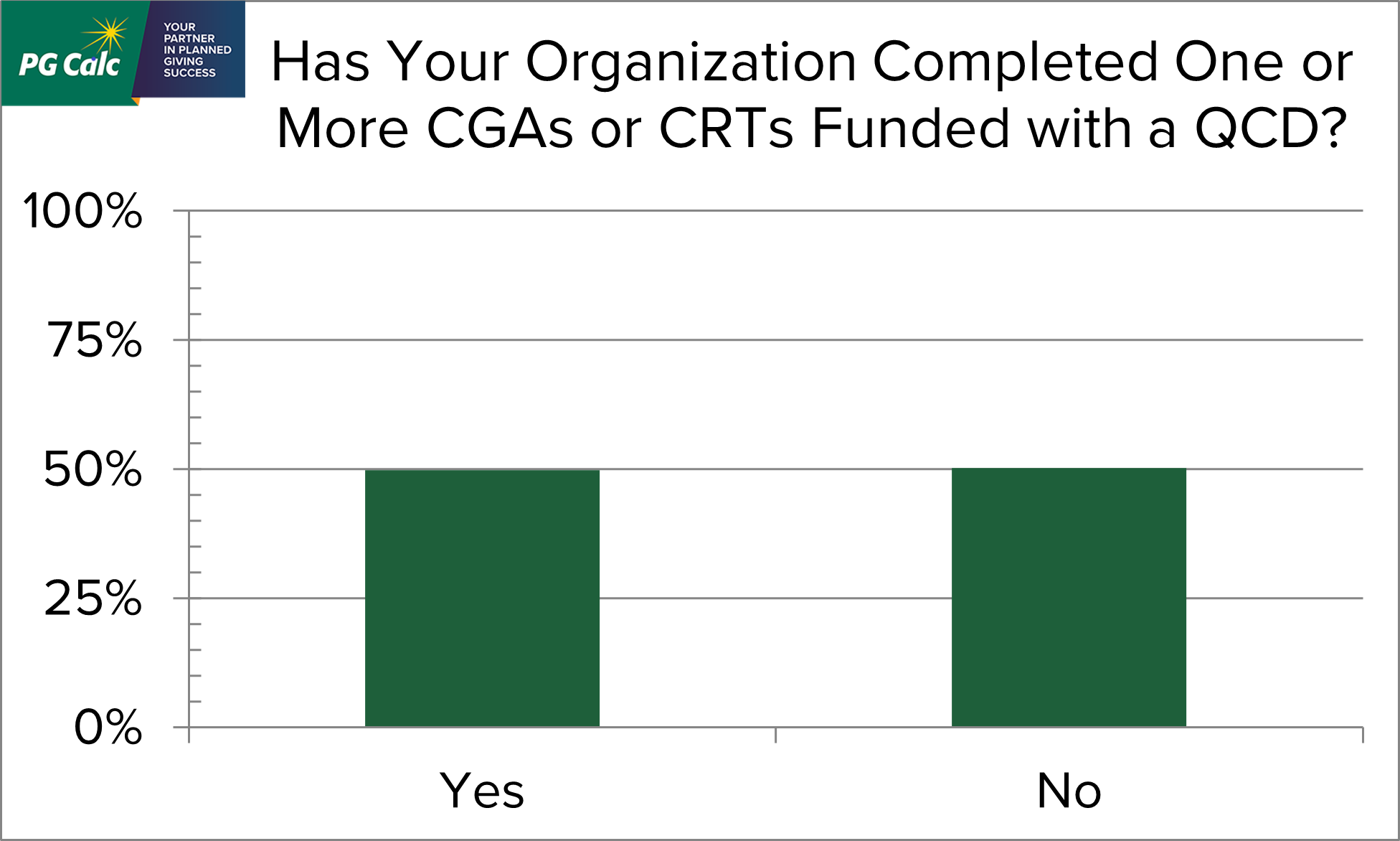

PG Calc QCD Survey: Many Charities Report Closing CGAs Funded With a QCD

-

A new gift planning opportunity became available at the beginning of this year thanks to the Legacy IRA Act that passed late last December: funding a charitable gift annuity (CGA) or charitable remainder trust (CRT) with a qualified charitable distribution (QCD) from one’s IRA. Gift planners were rightfully excited to have a new gift plan to talk about with their donors. However, the new gift plan’s many requirements raised doubts about how popular it would be. Who would make these gifts? Now that we are most of the way through 2023, the QCD for life income plan’s place in planned gift fundraising has become clearer.

A new gift planning opportunity became available at the beginning of this year thanks to the Legacy IRA Act that passed late last December: funding a charitable gift annuity (CGA) or charitable remainder trust (CRT) with a qualified charitable distribution (QCD) from one’s IRA. Gift planners were rightfully excited to have a new gift plan to talk about with their donors. However, the new gift plan’s many requirements raised doubts about how popular it would be. Who would make these gifts? Now that we are most of the way through 2023, the QCD for life income plan’s place in planned gift fundraising has become clearer.

In their interactions with clients, our Client Services and Gift Administration teams have noticed a recent increase in the number of new CGAs funded with a QCD. This pattern piqued our interest. To investigate the popularity of this new gift option further, we sent out a survey to a broad fundraising audience. We summarize our results below.

Measuring the Success of Your CGA Program: The Case for Maintaining Current Market Values for All Charitable Gift Annuities

-Charitable gift annuities (CGAs) are designed to be the split-interest gift for any donor. The basic premise is that the donor contributes cash or marketable securities to a charitable organization, and the charity promises to make payments to the donor for the rest of his or her life. The donor receives a charitable income tax deduction at the time of the gift, and some portion of the original principal remains at the donor’s passing.

That all sounds great, right? A classic “win-win-win” arrangement, and in fact, most charitable gift annuities result in a significant portion of the original principal as the residuum. When a charity has a robust gift annuity program, there can be enormous financial rewards from the ongoing stream of CGA terminations. But we’ve all heard the other side of the story as well. There are far too many examples where the gift corpus becomes completely used up, and in fact, the charity ends up kicking in money from general funds to continue making payments to an annuitant who lived beyond their original life expectancy. We call these “underwater gift annuities,” and they actually end up with negative dollar benefits.

So, what is the sum total benefit of this gift annuity venture from the charity’s perspective? Put simply, how does the charity even begin to measure the success of their CGA program?

Are You “Wasting” Your Time? Focus on Fundraising?

-Does this sound familiar? “I have to write the lead article for our newsletter by Friday. Where are those photos I want to use for the testimonial? What format should we use for our legacy society lunch? Should we hold the event at all? I need to get approval to the edits to our gift acceptance policies. Are we getting everything we are entitled to from that bequest?”

Read your job description. What is your primary responsibility? Does your title include Planned Giving Officer, Development Officer, Advancement Officer, Major Gift Officer, or similar terms? The principal concern and obligation of such a position is to attract voluntary support to advance the mission of a non-profit organization. But often, support functions prevent fundraisers from focusing on the most important part of their job: fundraising.

Funding CGAs with Mutual Funds – Is This Still a Problem?

-Americans have extensive holdings of mutual funds representing significant portions of their investment portfolios, and many invest exclusively in mutual funds. This makes sense – mutual funds are easy to purchase, simple to understand, and they allow for continuous reinvestment of dividends and income earned by the mutual fund shares. As donors review their financial assets to determine which ones to use to fund charitable gift annuities, mutual funds present an obvious choice. As an added bonus: mutual funds are easy to value for gift purposes. The share price of a mutual fund is determined daily and published as the “Net Asset Value (NAV).” A donor uses this share price to value a gift of mutual fund shares. In contrast, a gift of publicly traded securities must be computed as the average of the high and low trading prices on the date of the gift.

But gift planners should be aware of some particular aspects of mutual funds that can cause significant complications in the process.

Giving USA Report on Philanthropy: Is It the End of the World as We Know It?

-“Drop in Giving Among Steepest Ever,” screamed the Chronicle of Philanthropy headline. Other media piled on. The anodyne Associated Press led with, “Charitable Giving Drops, Only the Fourth Time in 40 Years.” And the redoubtable Barron’s reported, “Charitable Giving Falls for the First Time Since the Financial Crisis.”

Is this all just hyperbole? Or does it leave you wondering if it might be time to hang it up and consider a different career path? Don’t despair. At least not yet. The release last month of the 68th Giving USA Annual Report on Philanthropy (Giving USA Report), which reported a drop of 10.5% in giving last year, triggered the hoopla. The Report is an initiative of the Giving USA Foundation in collaboration with the Indiana University Lilly Family School of Philanthropy.

It’s too bad the Report has been reduced to a headline because, well beyond a simple scoreboard of giving, it also provides a wealth of useful information and interesting insights about the history of and trends in charitable giving in the United States.

Understanding Gift Tax and How to Minimize It

-While it may seem esoteric, understanding gift tax is very helpful if you’re working on a life income gift that benefits someone in addition to, or other than, the donor. In these situations, the donor is making two gifts: one to the charity and one to the income beneficiary, and this second gift may be taxable.

It is also helpful to have a basic understanding of gift tax when you’re discussing an estate gift, since gift tax and estate tax are linked together by the “Unified Credit.” This credit is applied to gifts that would otherwise be taxable transfers, whether made during lifetime or at death.

“Please, Sir, I Want Some More” - The Plight of Orphan DAFs

-What happens when there is money left in a donor advised fund after the last donor-advisor has died? Where does that money go? Who decides how the money is used? Like a street urchin in a Charles Dickens novel, an “orphan donor advised fund” can sometimes achieve great expectations or, sadly, pass invisibly without much impact. And, like Dickens’ obsession with orphans, there are those who are concerned about the growing orphan population and some who would exploit these orphans for their own purposes.

Partial Interest Gifts – Navigating Rocky Shoals and Avoiding Whirlpools

-Contributions of appreciated assets offer tax savvy opportunities for gift planning. But what if the donor is not eager to part with the entire asset? That’s no problem if the asset is securities; our donor simply transfers as many shares as she chooses and keeps the rest for herself. However, other assets aren’t so easily divided – things like real estate or bank, investment, or retirement accounts. A contribution of a partial interest can allow donors to give a portion of the property and retain the rest for themselves, their family, or others.

Navigating a contribution of a partial interest can be a bit like the challenges Odysseus faced on his journey home. It wasn’t all smooth sailing. He had to navigate rocky shoals, whirlpools, and angry gods, but eventually, he made it home safely.

Is Your Charity “Effective?” - Effective Altruism and Your Donors

-Recently, researchers at the Harvard Center for Brain Science crafted an experiment to see if donors could be redirected from supporting their favorite charities (“giving from the heart”) to supporting more effective charities (“giving from the head”). The effective charities were selected from GiveWell, a charity navigator for the Effective Altruism (EA) movement, which also funded the study through the Effective Altruism Fund. If your only familiarity with EA is its relationship to disgraced cypto-currency billionaire Sam Bankman-Fried, it’s worth learning a bit about the movement and how it’s working to change the nature of philanthropy.

EA encourages its followers to earn more, so they can give more and to support only the most effective charities with their giving. According to EA, an effective charitable gift benefits the most people for the least financial outlay.

Do you need to worry that EA will capture your donors? They’re certainly going to try.

That’s Alright – It Was Only Money (Putting 2022 in the Rearview Mirror)

-We’ve been saying for years that, when it comes to investments, charities should focus on the long-term picture. There are good years in the markets and bad years in the markets, but, with “prudent” investments, the long-term outcomes have been consistently positive. Whether it be the endowment assets of well-established organizations, or the investment portfolios of gift annuity programs and individual charitable remainder trusts, the general rule is to look at the bigger picture. But specific and dramatic swings in the investment markets – the stock market in particular – can have a chilling effect on donors with stock portfolios held over an extended period of time.

What do we say to the donors who have seen their investments lose significant value over the past 12 months or longer? And even within the organization, how do we respond to the more cautious voices among us who are spooked by double-digit declines in market values? We thought it would be helpful to take a look at the most recent investment performance measurements of mainstream investments.